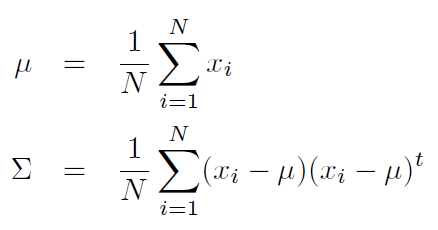

Mean and Covariance

Given samples of a class, x1, x2, ... xn, each being an d-dimensional vector, we define the mean, μ, and the covariance matrix, Σ are defined as:

Properties of μ and Σ

- Note that xis are d-dimensional column vectors, and hence the mean, μ, is also a d-dimensional column vector. The covariance matrix, Σ, is a dxd symmetric square matrix.

- The mean, μ is the centroid of the samples in the feature space.

- The covariance matrix, Σ is a positive semi-definite matrix.